Actionable competitive and market intelligence

Insights that matter for decisions that matter. Get the tools you need to successfully integrate top-tier competitive and market intelligence within your organization. Drive revenue growth, mitigate risks, and cut costs, propelling your business towards its objectives.

Surprisingly expected results from our customers

new, qualified sales leads weekly from untapped sectors and exclusive sources

deal won within a month of utilizing Valona competitor analysis tools

saved by timing a critical investment correctly with Valona’s market insight alerts

average order size increase through strategic sales opportunity screening with Valona

500+ companies already in the know

Preferred by top global corporations

Nothing beats covering all the bases

Valona’s competitive and market intelligence platform makes it easy to find, analyze, organize, and share the most relevant insights across every team in your organization. Blindspots will be a thing of the past.

See it in action

Nothing beats hybrid intelligence

With 20+ years of practical expertise in the market, experienced research consultants, and the most sophisticated AI to support them – get insights and strategic foresight to support decision-making across every function of your organization.

Read more

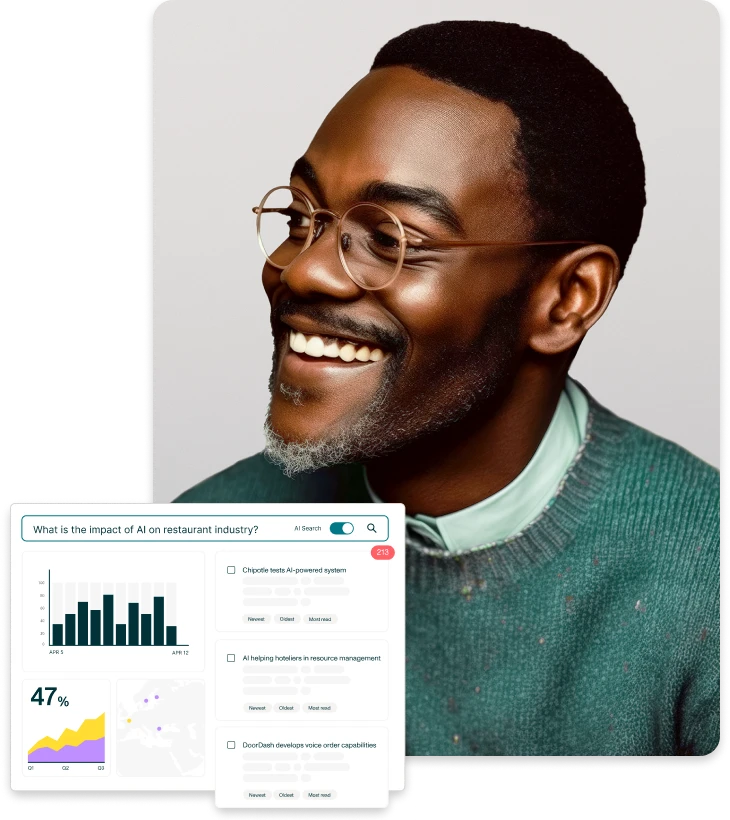

Nothing beats winning a new customer

Spotting early signals means your sales team will glide to victory. Catch warm sales leads from global sources you did not even know about, and become your sales team’s favorite colleague. They’ll thank you for the opportunity to seize every chance for business growth.

Read moreM-Brain is now

Valona Intelligence

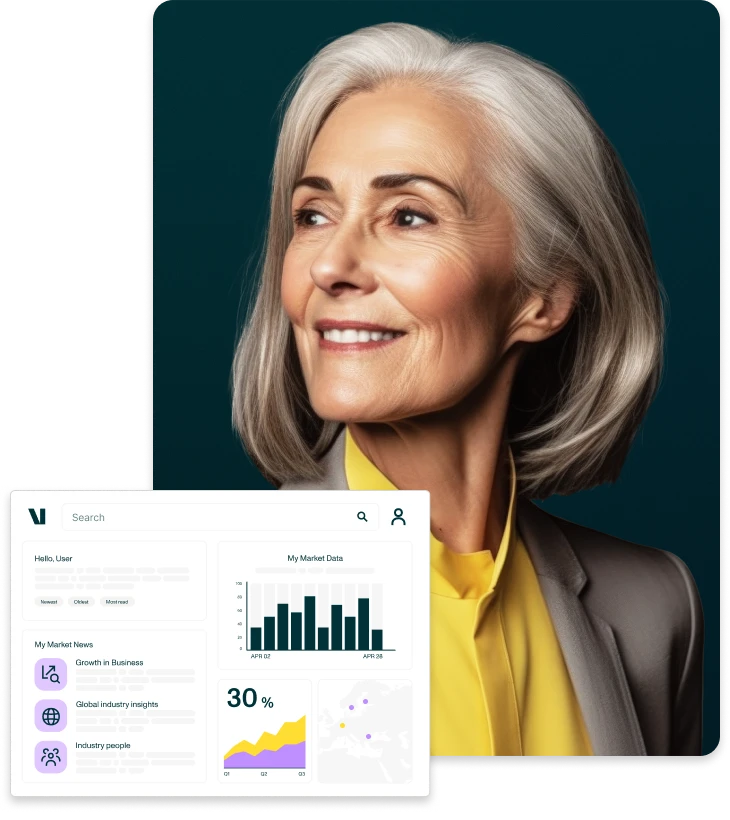

Nothing beats seeing the big picture

With the ability to see the forest from the trees, you can make impactful decisions across all departments and at all levels. Insights are the driver for competitive foresight. You’ll have AI tools for everything you need to shape the future and gain the competitive advantage.

Read more

Nothing beats staying ahead

With 20+ years of practical expertise in the market, experienced research consultants, and the most sophisticated AI to support them – get the insights and strategic foresight to support decision-making across every function of your organization.

Read more

Nothing beats waking up to fresh insights

With Valona’s AI Research assistant, it’s easy to keep your finger on the pulse at all times. Prevent big problems, stay informed about what’s happening in the world, and unlock sales opportunities while managing risk. Valona makes it as easy as opening your laptop in the morning.

Read moreBegin your success story with us

It’s your turn now. Connect with us to explore how Valona can equip you with the tools you need to grow your business, meet your growth targets, and expand to new markets.

Your journey to staying a step ahead starts here!